Considering refinancing your home? Refinancing usually saves money in the long run, and with interest rates hitting record lows, you’ll want to act quickly. In the following article, we’ll walk you through the refinancing process to help you determine a strategic time to refinance.

What is refinancing?

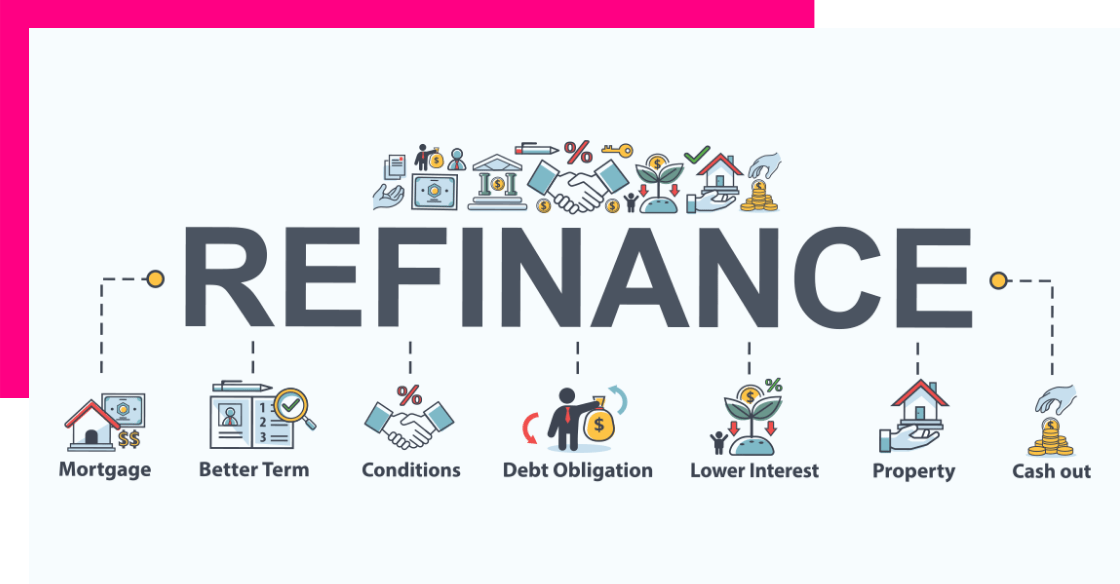

Let’s back up to review what refinancing is all about. “Refinancing” refers to the process of replacing an old mortgage with a new one. This is usually a smart move financially because it allows homeowners to take advantage of a current interest rate that is lower than the rate they agreed to when they signed up for the original mortgage agreement.

But you’ll need to take your credit history into account when weighing all the options. Borrowers with very strong credit scores who have an original mortgage with a “variable” loan rate (subject to the fluctuations of the market) may be able to convert their loan to a fixed rate, which means less guesswork and usually less money. Borrowers with lower credit scores or accumulated debt will need to strategize when refinancing to make sure the new rate is better than the original.

People choose to refinance their homes for many reasons: to reduce the amount they owe each month for a mortgage payment, to lower the overall interest rate of the loan, to take cash “out of” the home to help cover other large purchases, or simply to switch mortgage companies. Most people choose to refinance when they have “equity” on their home, which is the difference between the worth of the home and the amount that is owed through the home loan.

How do I get started?

If you suspect refinancing might benefit you, you first need to assess your current mortgage rate in order to determine the “Combined Loan to Value” (CLTV) ratio. This ratio is an indicator of whether you have “equity” on your home or not by comparing your mortgage loan balance to your home’s value. It takes into account all credit lines that you may have used to pay for your home. The percentage value is calculated by taking your current mortgage balance plus your potential home equity loan amount, then dividing that number by your home value. A lower number is better since that indicates a higher home value (denominator). A low CLTV percentage means you are in a good position to refinance your home.

When is the best time to refinance?

Deciding when to refinance can be tricky, depending on what’s happening with the market trends. While you should never refinance without considering all the factors at play, below are a few common reasons people choose to go through with refinancing.

1. You have an adjustable-rate mortgage

If you have an adjustable-rate mortgage (ARM), check when it is due to “reset.” These types of loans periodically can be switched to either a fixed mortgage or a different ARM, and usually, either option will save you money since it means that your rate would be guaranteed for a longer period of time (irrespective of what the market is doing). If you have an ARM and the reset period is coming up, do some research or consult a professional to determine whether refinancing will save you money long-term.

2. You have a higher income

Let’s say you were in an entry-level job when you first took out your mortgage, but after a couple of promotions, you are in a much better financial position. This ultimately means that your debt-to-income (DTI) ratio, which can increase your credit score (see point #3!). Having an income boost and a bump in your credit score almost always puts you at an advantage when it comes to refinancing.

3. Your credit has improved

If you were not able to get a competitive mortgage rate due to a low credit score, but your credit has since improved, consider refinancing! You likely qualify for much lower rates with a higher score. This sounds like an obvious one, but you’ll still want to weigh all the options before refinancing (do some research about market trends, etc.) since the credit score is just one factor in the equation.

4. You have other loans

Most people with a mortgage have also borrowed money elsewhere—whether it is via credit cards or student debt. The interest rates for these types of loans are usually much higher than home loans. If this is the case, and you are paying a significant amount of interest each month to cover the other loans, you can “consolidate” your loans so that you’re paying the same interest rates for all loans across the board. This can be done through the process of refinancing.

5. You live in a desirable location

When it comes to real estate, it all comes down to the home worth. That, in turn, depends on where you live. If you live in a location like San Diego where property values are steadily increasing, refinancing will likely work out in your favor.

Take advantage of dropping mortgage rates by digitally connecting with a mortgage broker to learn about your refinancing options.